Amid the constant battle with biology and new complexities in fighting disease, persistence seems to be paying off for drug developers. Major driving forces include the rise of CAR -T and other gene therapy, newly discovered cancer targets, better patient identification methods—and the realization that failures have their place in shaping the pipeline of tomorrow.

Pharmaceutical and biotechnology companies face similar problems. The targets are so enticing, the results often wanting. Consider checkpoint inhibitors. They are quasi-miracle drugs: incredibly powerful for the lucky responders, ineffective for others.

There are many variations on this theme. Following the success of cancer drug Gleevec, targeted therapies seemed like a sure thing. They’ve helped, but not as much as many had hoped. Pivoting to the central nervous system, the quest for effective Alzheimer’s disease therapies has been fraught with failure. Ask Merck & Co., Lilly, Axovant, Accera, Lundbeck, etc.

Many articles, including this one—Pharm Exec’s 14th Annual Pipeline Report—offer competitive snapshots, which companies have the upper hand. But in the end, the competition is with biology, which seems to be saying: “Really, you thought it would be that easy?”

But adversity is good for people and companies. The race is on to match checkpoint inhibitors with other therapies to transform cold tumors into hot ones. Companies’ researchers are reexamining their Alzheimer’s strategies. New targets are being tested in multiple indications. It seems the best way to meet complexity is with more complexity

But adversity is good for people and companies. The race is on to match checkpoint inhibitors with other therapies to transform cold tumors into hot ones. Companies’ researchers are reexamining their Alzheimer’s strategies. New targets are being tested in multiple indications. It seems the best way to meet complexity is with more complexity

Skepticism with Alzheimer’s

Bad news first. The Alzheimer’s Association projects there may be 16 million people with the disease by 2050, a crushing load for patients, caregivers, and governments. Statistics like this are generating a lot of urgency. Unfortunately, the pipeline keeps coming up short.

“There have been a lot of high-profile failures for amyloid plaque,” notes Joshua Pagliaro, partner in life science strategy at PwC. “I think a lot of people have had the question: Is this a sound scientific hypothesis?”

Pagliaro is not alone in his skepticism. “The amyloid theory may need some alterations,” says Les Funtleyder, portfolio manager at E Squared Asset Management and Pharm Exec Editorial Advisory Board member. “We may need to go back to the drawing board there.”

That’s not comforting for companies with amyloid therapies in the pipeline. They’ve gone this far, invested this much, they need to believe their science is better—their trial design superior.

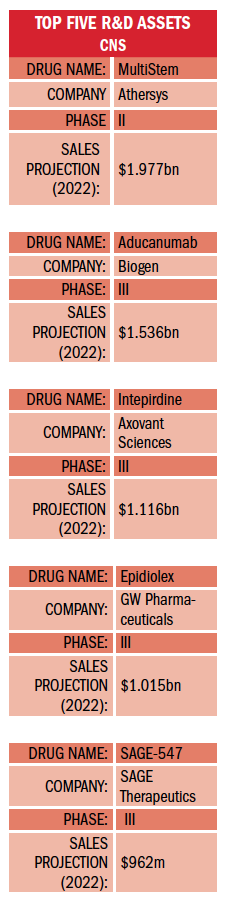

At present, Biogen’s aducanumab is being tested in two international Phase III trials (EMERGE and ENGAGE). The therapy, which targets beta amyloid, has been fast-tracked by the FDA. Recent findings in an extension of an early-phase study have been positive, showing the antibody therapy reduced amyloid plaque levels in patients treated up to 36 months. Given favorable results and ultimate approval, EvaluatePharma puts aducanumab sales at $1.5 billion by 2022.

Biogen has a particularly robust Alzheimer’s pipeline, including beta-secretase cleaving enzyme (BACE) inhibitor elenbecestat, which is being co-developed with Eisai. BACE inhibitors are designed to prevent amyloid plaques from accumulating. The drug has been granted fast-track designation in the US and is also in Phase III. Elenbecestat is projected to earn $296 million in 2022, mostly for Eisai.

In addition, Biogen is developing anti-amyloid antibody BAN2401, which is currently in Phase II trials. The company has a lot riding on the amyloid plaque hypothesis.

Amgen and Novartis have their own BACE inhibitor in the works, CNP520, a small molecule in Phase II, which has also been fast-tracked by the FDA.

AbbVie’s anti-tau antibody, ABBV-8E12, began Phase II studies early this year for Alzheimer’s and progressive supranuclear palsy. It has both fast-track and orphan-drug status in the latter indication.

Smaller vTv Therapeutics is in Phase III for its receptor for advanced glycation endproducts (RAGE) inhibitor, azeliragon. RAGE is upregulated in Alzheimer’s and is thought to play a role in inflammation, amyloid buildup, and tau phosphorylation. Azeliragon has a long checkered history, but is now moving forward.

Farther down the pipeline, companies like Cognition Therapeutics are trying different approaches. The company’s investigational drug CT1812, a small molecule that targets sigma-2 receptor complex on neuronal synapses to mitigate amyloid toxicity, was recently fast-tracked by the FDA.

These organizations may have better success with their Alzheimer’s therapies, or the industry may have to rethink its strategies.

“Some of the challenges have been around patient recruitment,” says Pagliaro. “We’re recruiting patients who have early signs and symptoms already. Is that really the right time to treat? Should we be treating Alzheimer’s prophylactically, like the way we treat cardiovascular disease?”

Given the development of accurate biomarkers, this could be a sound strategy. On the other hand, are private payers going to pay top dollar for prophylactic therapies when Medicare reaps the ultimate financial rewards?

For now, companies with Alzheimer’s therapeutics in late-stage trials are sweating it out. They’ve seen the carnage, are they next?

MS and epilepsy

Multiple sclerosis (MS) therapeutics offer a brighter picture. And, yes, this is cheating, since MS can be considered more autoimmune than CNS disorder.

Celgene’s ozanimod is one of the brighter spots in the pipeline. The oral, selective S1P 1 and 5 receptor modulator is in Phase III for relapsing MS, ulcerative colitis, and Crohn’s disease. In May, Celgene announced positive results for the RADIANCE trial. The drug’s safety profile may give it a leg up on Novartis’ fingolimod. EvaluatePharma predicts ozanimod could produce $1.4 billion in sales by 2022.

Novartis is not blind to fingolimod’s shortcomings and is working on its own next-generation S1P modulator, siponimod, which could generate fewer side effects. The drug is currently in a Phase III trial for patients with progressive MS. Evaluate estimates siponimod’s 2022 sales at $915.6 million.

Actelion, now part of Johnson & Johnson, is testing its S1P drug ponesimod with Tecfidera for patients with relapsing MS. Tecfidera is approved to treat psoriasis.

Epilepsy is one of the specialty markets that is getting much attention. GW Pharmaceuticals leads the way with its cannabinoid product Epidiolex, which treats Dravet syndrome, Lennox-Gastaut syndrome, and other severe forms of epilepsy. Epidiolex is in Phase III for both indications, as well as tuberous sclerosis, and has received orphan designation from the European Medicines Agency (EMA). Evaluate estimates Epidiolex’s 2022 sales at $1 billion. Despite delays, the drug seems poised for FDA approval.

GW’s picture brightened when Sage Therapeutics’ GABA modulator, SAGE-547, for super-refractory status epilepticus, failed recently in Phase III. The company continues to look for ways to move the drug forward, perhaps focusing on patient subgroups.

Zogenix recently announced positive Phase III results for its Dravet syndrome treatment, ZX008, which took some of the luster off GW. The drug is low-dose fenfluramine hydrochloride, a serotonin booster. It was both effective and well-tolerated. ZX008 has received orphan-drug designation from both the FDA and EMA. It has also been fast-tracked in the US for Dravet syndrome. Evaluate estimates sales of $219 million in 2022.

Another interesting specialty market is migraine. Novartis and Amgen are co-developing the monoclonal antibody erenumab (AMG 334 or Aimovig), which is in Phase III studies for episodic and chronic migraines. Erenumab targets the calcitonin gene-related peptide (CGRP) receptor to block pain. A recent analysis from Novartis showed the drug reduced the number of migraine days by as much as 50% for patients who failed previous preventive therapies. Amgen has exclusive commercialization rights in Japan; Novartis has exclusive rights everywhere else.