Global health is poised to meet a series of key turning points, and changes seen in 2018 will mark the key inflections that drive the outlook for the next five years and beyond. The types of medicines being developed, the way technology contributes to health, and how the value of healthcare is calculated are all markedly changing.

Innovation is a key theme, including the way regulators of medicine and applicants filing for approval will increasingly support clinical submissions with real world data. A wave of cell and gene therapies are bending the definition of what constitutes a drug, both clinically, and in terms of expectations of outcomes, duration of treatment and costs.

Technology itself can be a treatment, and mobile apps are newly appearing in treatment guidelines as a key feature of future care paradigms. Furthermore, mobile technology can be an enabler of telehealth communication that brings providers and patients together at substantially lower costs than traditional consultations.

In recent years, concerns about escalating medicine costs have captured significant attention. In 2018, some of the key drivers of medicine spending growth appear to be slowing spending rather than driving it upward. The causes of slowing growth are directly linked to payers concerns about budgets and to newly emerging mechanisms to adjudicate value and thus limit the potential for out-of-control spending growth.

Key Findings

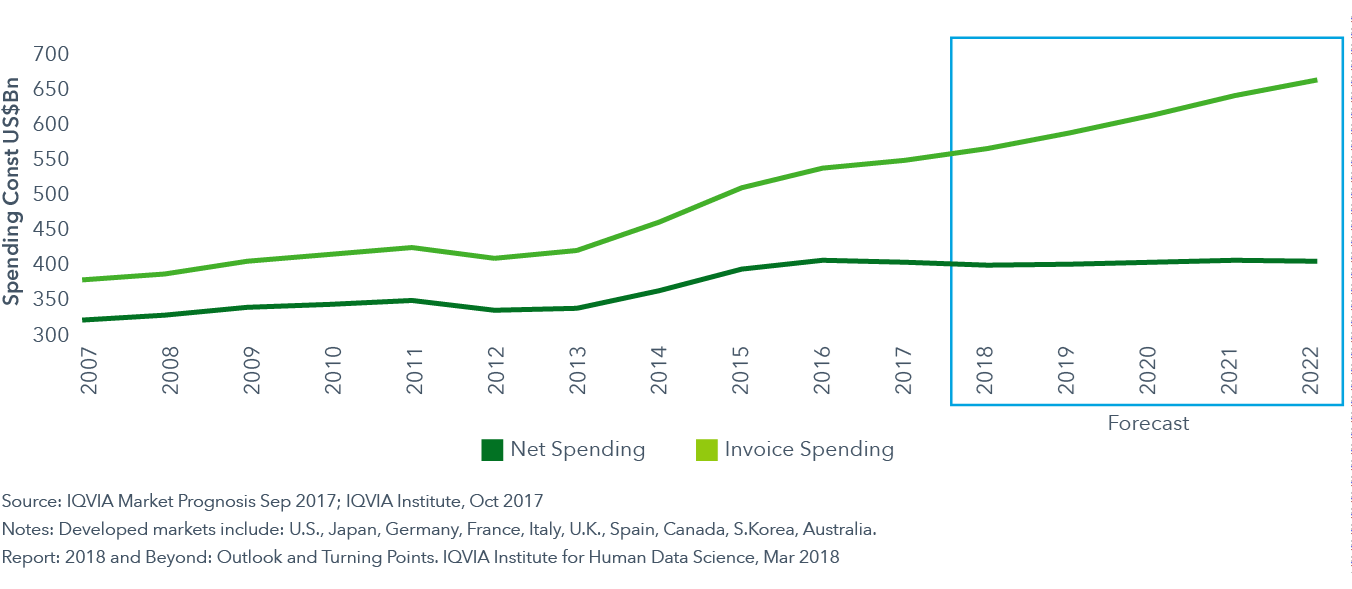

Invoice spending in the developed markets will reach over $650 billion by 2022, while net spending will remain flat

- Over the past five years, branded drug net spending in developed markets has risen from $326 billion to $395 billion. In total, 87% of the $69 billion of net growth has come from the United States.

- In 2018, net brand spending will decline in developed markets by 1-3%. This has the effect of reducing net spending overall on brands in developed markets by approximately $5 billion to a total of $391 billion in 2018.

- While the absolute share of spending from new medicines may be small, control of pricing and access to new drugs is a key point at which payers can influence drug spending trends for the longer term.

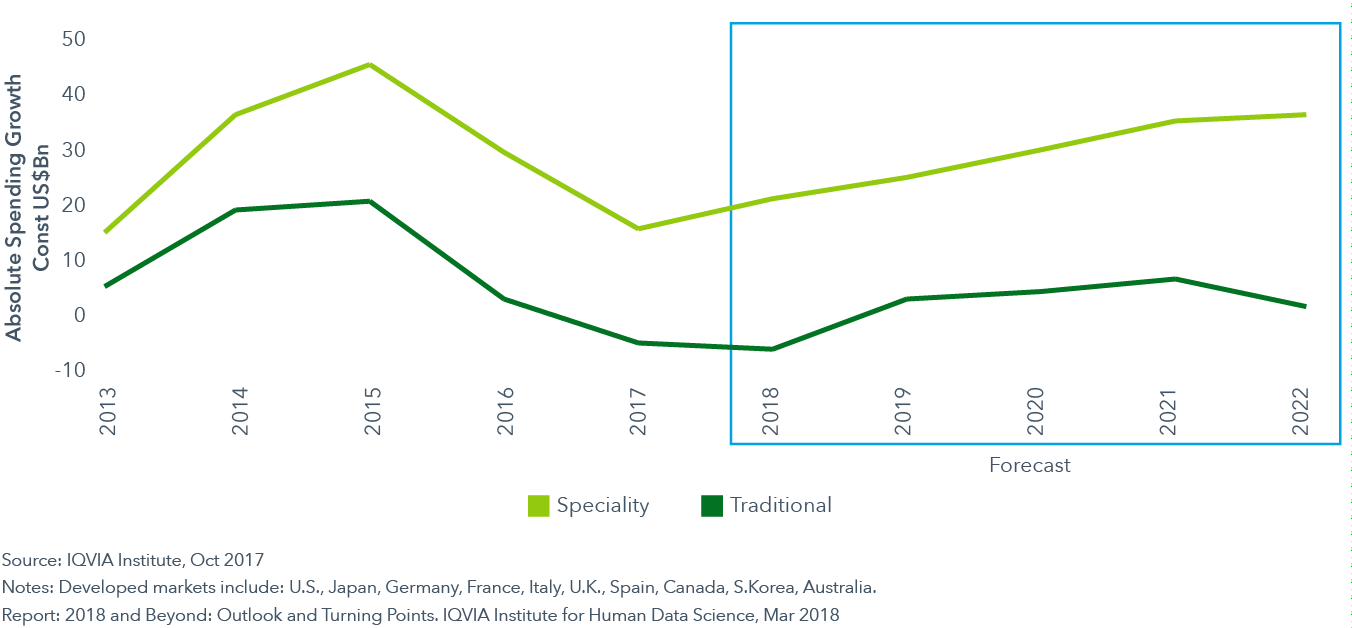

Branded specialty drugs will drive all growth in 2018, while traditional growth declines

- The past decade has seen a sustained shift in the focus of new medicines towards specialty pharmaceuticals. These are defined as those medicines treating chronic, complex or rare conditions, among other criteria.

- Specialty share of global spending has risen from 19% in 2007 to 32% in 2017. For the tenth consecutive year, specialty medicine growth exceeded traditional medicines in developed markets. In the ten developed markets, specialty represented 39% of spending in 2017, totaling $297 billion.

- Specialty share in developed markets will continue to rise, albeit more slowly than the last few years, and surpass half of medicine spending in 2022 in the United States and in four out of the five key European countries: France, Germany, United Kingdom and Spain.

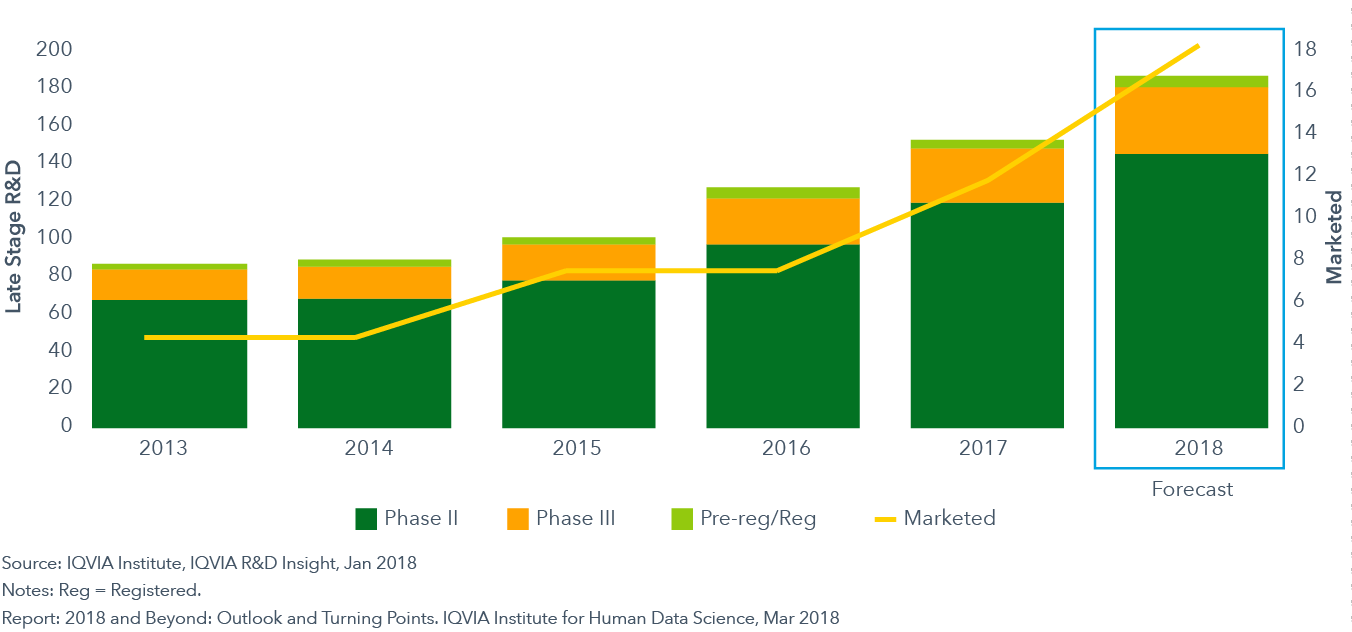

The number of Next Generation Biotherapeutics in the pipeline and market is set to rise

- Next Generation Biotherapeutics include the latest generation of cell-based therapies, gene therapies and regenerative medicines.

- In 2018, between five and eight Next Generation Biotherapeutics will be approved and launched and, over the next five years, these therapies will make up 20% of the 40-45 New Active Substances (NAS) projected to be launched each year.

- In most cases, Next Generation Biotherapeutics will have costs approaching or exceeding $100,000 per patient. The challenge both for manufacturers and payers will be to create a new payment and reimbursement paradigm that maximizes access to these new therapies.

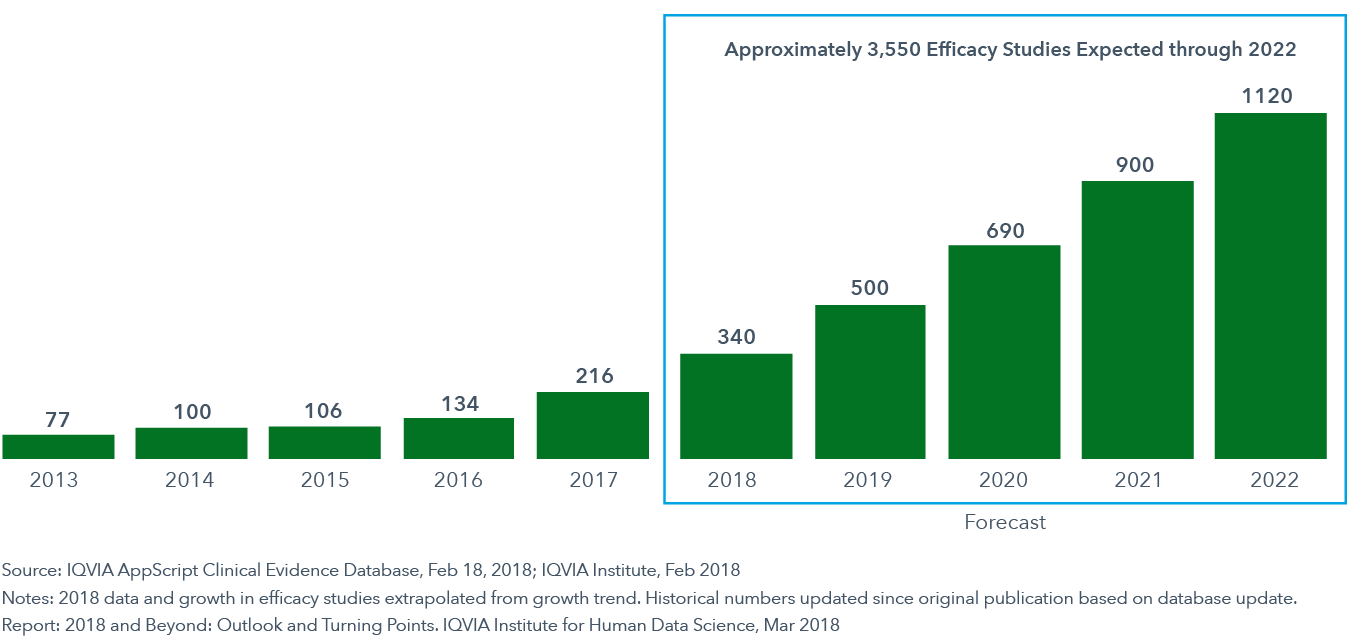

Published evidence of digital health will increase over 500 percent through 2022

- In 2018, approximately 340 digital health efficacy studies will be completed and published, continuing the trend of building hard evidence to support digital tools and interventions.

- An acceleration of evidence building will bring an estimated 3,500 studies over the next five years and the incorporation of apps by major professional groups into practice guidelines.

- Alignment on the appropriate sets of features and safeguards for apps has emerged and technology innovators are advancing into the field in significant numbers. Integration with provider workflows that occur in the next five years will be critical to stakeholder adoption.

- The emergence of well-designed apps and mobile devices offers the potential to improve outcomes for patients, sometimes at near-zero incremental costs.